In the article “Study could lower or nix local flood insurance costs” we see a familiar situation that was finally resolved by ONE citizen paying for a flood study to help his neighbors. The situation was that…

Residents along Wolf Creek used to see more flooding until two dams along the waterway at North Street in Pine and East Main Street in Grove City were removed 11 and 12 years ago, respectively, and the waters have receded significantly. Since that time, the residents believe their insurance is no longer justified – or could at least be reduced.

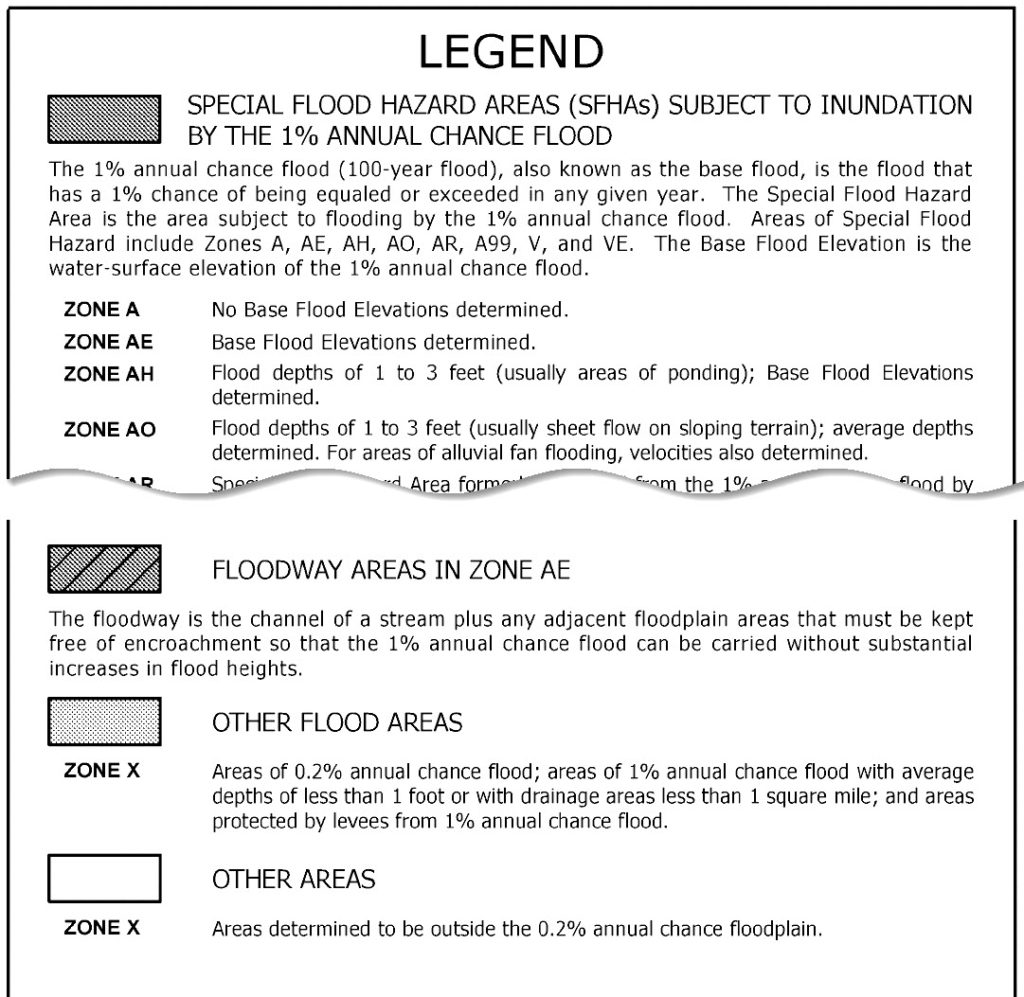

Flood Zones Explained

FEMA’s Flood Insurance Rate Maps (FIRMs) determine the flood insurance rates that FEMA charges landowners who are located in a Special Flood Hazard Zone. This is also known as the 1% Chance Storm Flood Zone and is typically designated as Zone AE. The “E” means there is a Base Flood Elevation that has been established.

There are 3 situations you may find yourself in on a flood map:

- Out of the flood hazard zone completely, the best situation. This is usually designated as “X Outside the 0.2% Chance Flood Zone.” In this case you are not required to purchase flood insurance, though you may consider doing so if you have a wet weather drain close to your house.

- Your lot and/or house is shown in Zone “X Within the 0.2% Chance Flood Zone.” In this case you are also not required to purchase flood insurance but it is highly advisable. The 1% storm event is exceeded in many cases. (The water doesn’t know that it’s supposed to stop at that elevation.)

- A portion of your lot and/or home is shown in the flood hazard zone on the Flood Maps. This requires flood insurance, or proof that the maps are inaccurate. At this point your home may or may not be actually below the Base Flood Elevation, the 1% chance flood elevation.

- Your lot is IN the flood zone, but your house and the Lowest Adjacent Grade (LAG) next to it is OUT, or ABOVE the Base Flood Elevation. This has to be determined by a land surveyor. If so, you may qualify for a LOMA to remove the requirements for flood insurance.

- Your house and/or the Lowest Adjacent Grade (LAG) are BELOW the Base Flood Elevation. You won’t qualify for a LOMA. Get an Elevation Certificate by a land surveyor in order to determine your flood insurance premium.

A Fourth Flood Map Situation

A Fourth Flood Map Situation

In this article, a FOURTH situation is given; you are shown IN the flood hazard zone on the current maps but something has changed since the map was published that would show you to actually be OUT of that hazard zone. In this case, a flood study has to be undertaken to prove to FEMA that something has changed. Unfortunately this flood study has to be paid for by someone. If your City and/or County won’t do it, then it is up to you or your neighbors to undertake this study.

A Flood Study

A flood study is done by engineers who are trained and licensed to undertake these tasks. A flood study involves calculating the height which the 1% chance storm will rise to as it flows through the stream. You do this by taking measurements of the shape of the stream at various locations and determining the amount of water that will runoff the overall drainage area, and how fast it will get to that segment of the stream. Honestly, there’s a LOT of estimating done for this kind of work, but it’s at least educated estimating. (I refrained from saying educated guess because that would diminish my Auburn education. War Eagle!)

Flood Study Costs & Facts of Life

The flood study in this article ultimately costs over $35,000. In my experience, the minimum flood study cost I’ve seen is in the $5000 range. It could run much higher, but that would usually involve a large area.

Unfortunately when most people are in this Fourth Situation, neighbors won’t cooperate and share the cost. I believe personally that the city or county should incur these costs, but in most cases, there aren’t funds available for this. And, since it involves a small segment of the people, it is usually not justified by people who were voted into office.

Another possible way to fund a flood study is through a Tax Assessment from the jurisdiction involved. This would require the individuals who are helped by the flood study to pay up when and if they sell their home. The idea is that being out of the flood zone would mean they get a higher price for their home than if it was still in the flood hazard zone.

![]()

Keith Maxwell is a Professional Engineer & Land Surveyor who has done flood studies in the past, but he got paid to do them, except for one who was a deadbeat client.